Resistance is Simple, Resilience is Complex: Sanctions and the Composition of Iranian Trade

ESFANDYAR BATMANGHELIDJ

OVERVIEW

This paper challenges the conventional wisdom that the multilateral and unilateral sanctions imposed on Iran since 2008 have isolated it from the global economy. Multilateral sanctions did slow many of its economic processes associated with globalization, particularly attraction of foreign investment and technology. As relations with the West worsened, Iranian officials adopted the rhetoric of a “resistance economy,” leading many analysts to believe that their economic doctrine was diametrically opposed to globalization, rejecting the world in response to the world’s rejection of Iran. However, an analysis of trade data for 2009-2018 makes clear that rather than reject globalization outright, Iranian economic actors responded to sanctions pressure with strategic and conditioned choices around geography and product that made the composition of trade more complex. In turn, the emergence of greater geographic and product complexity made the economy more resilient to sanctions pressure, with the continued flow of critical imports and exports enabling the manufacturing sector to sustain production and employment. That Iran achieved economic resilience in the face of sanctions through greater, not less, engagement with the global economy indicates important opportunities for future economic diplomacy.

I. INTRODUCTION

The development of the “resistance economy” (eghtesad-e moghavemati) emerged as a major feature of Iranian political discourse following the intensification of multinational sanctions around 2011. That discourse found renewed salience after the Trump administration’s imposition of “maximum pressure” beginning in 2018. Proponents argue that Iran can best resist the economic pressure of sanctions by the related processes of import substitution and indigenization of technology. Iran’s Supreme Leader, Ali Khamenei, has described a resistance economy as one that “boils from within.” The persistence of this rhetoric, reflected in public statements of a wide range of officials, has given rise to belief that the economy has grown more autarkic under sanctions, with a high degree of self-isolation characterizing policymaking.

But the political rhetoric of resistance, which posits responding to sanctions with self-sufficiency, does not reflect the reality of Iran’s economic response. Policymakers have taken steps to encourage import substitution, principally by introducing import duties, but the economy today is more open to global trade than ever before. In recognition of this, some Iranian economists and policymakers have started to stylize the phrase eghtesad-e moghavamati in English as “resilience economy,” so as to describe the economic response to sanctions in ways that diverge from resistance rhetoric. This paper examines the trade policies and patterns that underpin the resilience economy. It builds on a small but important body of research that identifies Iran’s response to sanctions not as embracing isolation, but as further embracing the economic processes at globalization’s heart.

Looking to Iranian trade’s composition over the last two decades, several features stand out. Notably, the economy showed significant non-oil export growth, partially compensating for the fall in foreign exchange revenue as sanctions dramatically reduced oil revenue. The growth in non-oil export revenue resulted from an increase in complexity. First, the composition of trade began to show more geographic complexity, that is, a wider range of export destinations. Secondly, it began to exhibit greater product complexity: an increase in the range of products among non-oil exports. The emergence of greater economic complexity, particularly in trade, means that the study of Iran’s response to sanctions can be posited within a wider body of work of economists who trace the relationships between economic complexity and growth [1]. Of course, greater export complexity was predicated on a similar increase in import complexity, in both products and geography. For manufacturers to produce a wider range of products marketable to a more countries, it was necessary to import a wider range of raw materials and intermediate goods.

An examination of trade data tells the story of Iran’s embrace of trade complexity as part of its resilience under sanctions strategy. Sanctions have had a significant deleterious impact on economic growth, leading to a decade of stagnation. But absence of growth does not indicate absence of development, and the steady expansion of non-oil exports, totaling $41.2 billion in the Iranian calendar year ending in March 2020, points to a largely unheralded example of economic development [2]. The political implications of this are profound, given the ways in which the economy remains, despite a decade of intense sanctions, fundamentally oriented toward the global economy.

II. (MIS)PERCEPTIONS OF ISOLATION

Evocation of the resistance economy has been a feature of Iranian political discourse since the founding of the Islamic Republic in 1979. The eight-year Iran-Iraq war, which began in 1980, required mobilization of a war economy. The resistance economy idea found heightened political salience as Iran was subjected to a broad, multilateral sanctions campaign, beginning in 2008, that ended a fruitful, decade-long period of industrialization enabled by international, particularly European, investment. During that decade of growth and technological advancement, policymakers sought to grow non-oil exports. The long tension between the priorities of developing domestic industrial capacity and expanding opportunities for trade was settled within the context of the Vision 2025 development plan launched in 2005, which definitively targeted a role for Iran in regional and wider international markets [3]. But a few years later, sanctions threatened to turn the country’s focus away from trade. The resistance economy idea reemerged, particularly in the Supreme Leader’s decrees. By 2012, as the country experienced a 7.5 percent economic contraction, officials, including the Supreme Leader and President Ahmadinejad, were speaking of an “economic war” imposed by the West and urging Iranians to support the resistance economy [4].

The economy’s poor state and the sanctions challenge loomed over the 2013 presidential elections, with candidates forced to articulate their plans to resist pressures on the economy [5]. The victory of Hassan Rouhani indicated that Iranians were not content to resist sanctions through isolation and sought to normalize relations with the West. Six months after Rouhani’s inauguration, in February 2014, the Supreme Leader introduced the “general policies” of the resistance economy, the first detailed explication of the doctrine. His speech, which can be regarded as a kind of decree, reiterated the importance of developments in domestic production, improving the quantity and quality of output so as to reduce demand for imported goods. But it also included policies that indicated an evolution in the resistance economy idea and presaged the pursuit of negotiations to resolve the nuclear dispute and achieve sanctions relief. As noted at the time, most of Khamenei’s objectives could be considered “part of an economic liberalization program” and reflected “very few goals and reform objectives that are unique to Iran’s specific ideological context” [6]. The general policies included calls for government to promote export of goods and services by reducing red tape and to improve Iran’s attractiveness as a destination for foreign investors, objectives that Khamenei had previously endorsed as part of the Vision 2025 development plan.

This nuance was lost on most foreign observers. Continued use of the term “resistance economy” by figures such as Khamenei led many to conclude that economic policymaking was paralyzed by an internal debate between those seeking more openness and those who believed that “the more Iran becomes entangled in the global economy, the less it may be willing to challenge the West” [7]. But, as was smartly observed in 2013, characterizations of Iran’s “attitude and posture towards the global economy as wholly distrustful, apprehensive, or critical would be a simplistic stance....The Islamic regime’s approach to the international economy has in reality been more complex and contradictory than may be characterized as ‘anti-imperialist’, autarkic, or disengaging” [8].

While the slogan remained the same, evolution of the resistance economy’s general policies, as articulated by Khamenei and others, reflected the fact that whatever the apprehensions among politicians, the economy’s composition had changed in the six years between the imposition of multilateral sanctions and Khamenei’s February 2014 speech. This change — most evident in the country’s burgeoning global trade — indicates that economic policymaking in Iran is not exclusively, or even primarily, a top-down process. Rather, policies often emerged bottom-up, reflecting firm-level decisions in response to both internal and external pressures. In the case of trade, manufacturers did not respond to sanctions on their supply chains by embracing isolation.

The push for economic complexity began in earnest in the early 2000s, when Iran began to engage with globalization, which can be understood as a set of processes that generate economic complexity. Iran benefited from trade liberalization, integration into global logistics networks and introduction of foreign capital and technology. Manufacturers began to produce new, higher quality products, initially intended for the large consumer market, but as local firms and local joint ventures gained market share (often at the expense of imported goods), they began to target export markets. In 1998-2008, when, like many developing economies around the world, Iran experienced globalization, the composition of its trade was characterized by increased geographic complexity. In 1998, Iran had just 98 export partners and 67 import partners. A decade later it was exporting goods to 157 countries and purchasing them from 119 countries — growth that speaks to the remarkable forces of globalization.

Following imposition of sanctions, many processes associated with globalization may have slowed, particularly the introduction of foreign investment and technology. Fixated on the political rhetoric, much Western analysis came to see the resistance economy doctrine as diametrically opposed to globalization, believing that Iran had rejected the world in response to the world’s rejection of Iran. However, the pursuit of economic complexity did not stop, so it can be said that rather than reject globalization, Iran pursued a different kind of globalization: firms, and later policymakers, found themselves seeking greater complexity through strategic and conditioned choices around product and geography. This is clear in the absolute value of imports and exports. Between 1998 and 2018, exports rose from $14.5 billion to $85 billion, while the share of exports of petroleum products and natural gas fell from 79 percent to 64 percent. Excluding these hydrocarbon products, exports rose from $3.1 billion in 1998 to $25 billion two decades later. Imports also grew significantly, from $12.4 billion in 1998 to $54.6 billion in 2018, the last year for which comprehensive data is available.

This paper draws on data compiled by UN COMTRADE in order to focus on individual product categories [9]. The data can be imprecise, particularly given the importance of trade with regional countries and the significant volume of informal trade not captured in customs statistics. Nonetheless, the data illustrate the emergence of geographic and product complexity in the composition of Iran’s trade and explain how these trends relate to the pressure of sanctions on the economy.

III. GEOGRAPHIC COMPLEXITY

The imposition of multilateral sanctions beginning in 2008, culminating with financial sanctions in 2012, impacted many trade relationships. Despite the popular conception of sanctions as a kind of embargo, most countries did not stop trading with Iran in response. Many categories, such as trade in foodstuffs and consumer goods, were not directly impacted by the sanctions. Moreover, not all countries were equally deterred by sanctions from maintaining commercial links.

For Iranian policymakers, the question of sanctions response was about identifying which trade partnerships would prove most sensitive to the pressure. That sensitivity is a function of several factors, including the level of political alignment with the U.S. and Europe, the degree of financialization in the economy (and therefore exposure to risks emanating from U.S. primary sanctions), and the extent to which goods typically traded are subject to sectoral sanctions. In order to conceptualize these degrees of sensitivity, Iran’s major trade partners can be placed in three categories: those highly sensitive to sanctions (such as European Union (EU) member states; those somewhat sensitive (such as China and India); and those which are insensitive (such as Iraq and Afghanistan).

The importance of geographic complexity for Iran’s economic resilience under sanctions is most clearly demonstrated by looking to the relative growth of exports to countries in each category. Growth to insensitive countries relative to highly sensitive ones shows how the geographic composition has changed in response to sanctions. Sanctions accelerated the rate at which the overall value of exports to somewhat sensitive countries overtook those to highly sensitive ones, a trend exemplified by China’s emergence as Iran’s leading trade partner, overtaking the EU (Chart 1).

In 2009, the first year for which complete data is available in all three categories, the value of exports to somewhat sensitive and highly sensitive countries was about equal at around $28 billion. By 2018, exports had declined to highly sensitive countries to just under $19 billion, while to somewhat sensitive ones they were $52 billion. In the same period, exports to insensitive countries rose from $6 billion to $13 billion. Within this category, Iraq’s emergence as a key export destination is particularly notable. While exports there were just $4.5 billion in 2009, when Iran was sending $13 billion of goods to the EU, they had risen by 2018 to just under $9 billion, while exports to the EU had fallen to $11 billion. In this way, the emergence of regional markets as part of the geographic complexity of Iranian exports has helped compensate for the diminished prospects in countries highly sensitive to sanctions.

Growth in exports to insensitive countries has outpaced the other categories, with the value of exports rising 121 percent between 2009 and 2018. In the same period, exports to somewhat sensitive countries rose 81 percent, while to highly sensitive countries they fell 44 percent (Chart 2).

Discussion of how sanctions hit exports tends to focus on the oil industry, since Iran’s economy is misperceived as being dominated by that industry. Sanctions did have a significant impact on global demand for Iranian oil. Given global fluctuations in the oil price, a useful proxy for demand for Iranian oil is the difference between Iran’s oil production and consumption levels. That difference fell from 2.6 million barrels per day in 2011 — the year the US first imposed broad sectoral sanctions on Iran’s oil — to 1.6 million barrels per day in 2013. The difference between the two figures in 2019 — the first full year after the Trump administration re-imposed secondary sanctions — was 1.5 million barrels per day (Chart 3).

In both periods, Iran’s domestic market for crude oil exceeded its international market, a reversal that reflects the change in the country’s fortunes, and also how its large domestic market differentiates it from other Middle East oil producers. For the last two decades, domestic consumption has remained relatively stable, indicating that lower production principally reflects reduced export demand. Sanctions’ success in reducing demand for Iranian crude oil was the greatest single driver of the decrease in overall export revenue. Still, Iran found ways to use complexity to its advantage in order to respond to this reduced demand. Domestic consumption included the development of a greater downstream production capacity, allowing Iran to partially compensate for reduced oil exports by production and export of derivative products, such as plastics.

Also notable is the divergence between export growth across the three categories of countries. Prior to sanctions, most demand for Iranian oil came from among the highly sensitive. Among the somewhat sensitive ones, only China and India count among Iran’s largest buyers. When the EU imposed an outright ban on Iranian oil purchases in 2011, Tehran’s goal became to sustain the lower level of exports still going to Asian customers. Under Obama-era sanctions, these Asian oil customers were permitted to sustain a lower level of imports on condition that Iran’s earnings would be paid into escrow accounts and be available only to buy humanitarian goods such as food and medicine. This is one reason why exports to highly sensitive countries (including the EU) fell, while those to somewhat sensitive countries showed some growth. The Trump administration permitted a similar accommodation until May 2019.

While insensitive countries have emerged as a major export destination, they have not proven an alternative imports source for Iran, as sanctions limited trade with traditional suppliers. Imports from insensitive countries remain minuscule, just $203 million in 2018 (Chart 4). Growth has been a negligible 4 percent between 2009 and 2018. These figures reflect how insensitive countries, while offering a destination for exports and opportunity to generate export revenue, cannot supply the raw materials and intermediate goods Iran needs to sustain its industrial output. This is particularly true when considering the importance of machinery and equipment imports: goods that are not generally produced in insensitive countries, which tend to have lower levels of economic development.

At best, Iran has been able to shift some of its reliance on imports from highly sensitive countries to somewhat sensitive ones, either sourcing parts and machinery produced in those countries (as with Chinese goods) or relying on re-exports from them of parts and machinery produced in highly sensitive countries (as with the re-export of European goods through the UAE).

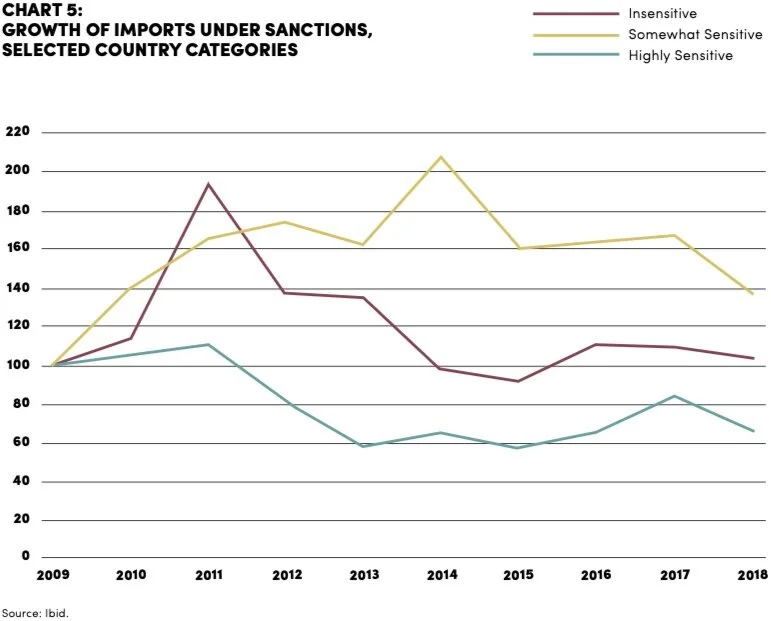

The value of imports from highly sensitive countries fell 35 percent between 2009 and 2018, reaching a nadir in 2013. Meanwhile, imports from somewhat sensitive countries grew 40 percent, peaking in 2014, around the time when imports from highly sensitive countries were most restricted (Chart 5).

Looking across exports and imports, Iran’s foreign exchange earnings under sanctions have not always kept up with its spending. Under sanctions, given the propensity to sustain imports, Iran tends to run significant trade deficits with highly sensitive countries; such deficits have also become a more pressing concern with somewhat sensitive countries (Chart 6). They place enormous pressure on Iran’s foreign exchange market. With its exporters struggling to earn and repatriate foreign exchange earnings, its importers are left to scramble to secure the euros, and lately the renminbi, necessary to pay for goods. Iran has large reserves with which it could conceivably finance these deficits, but sanctions have limited the ability of its Central Bank to freely use the funds, even for humanitarian trade. In October 2020, the International Monetary Fund estimated Iran’s reserves at a substantial $88 billion, but noted that just 10 percent was “readily available and controlled” [10].

These trends have worsened in the face of the Trump administration’s sanctions, particularly as China has reduced direct imports from Iran. For the first time, Tehran has a trade deficit with China, though this does not account for the value of Iranian oil re-exported to China via Malaysia [11]. In any case, even if Iran has a growing trade surplus with insensitive countries, it will face a significant challenge to finance trade deficits denominated in euros and renminbi. The only remedy is to begin exporting sanctions-exempt goods to the EU and China in far greater volumes. But while the composition of trade has changed in response to these pressures, registering significant growth in non-oil exports, the new product complexity has not helped avoid trade deficits. Iran may be selling more products to more countries, but its exporters are not yet managing to sell the right products to countries where they need to earn the most.

IV. PRODUCT COMPLEXITY

Iran’s ability to sustain the geographic complexity of its trade relations was not entirely the result of state planning. The geographic complexity that emerged in global trade in the first decade of the millennium was itself a result of the state’s diminished role in such trade. Iran could not simply count on sympathetic governments to keep goods flowing in the face of sanctions. To sustain trade relationships, it needed to bring the right products to global markets. Its major trade partnerships had long been anchored to oil. Oil sales to Western Europe, China, India and Japan, among others, gave the means to purchase goods from those countries. But with oil sales particularly vulnerable to sanctions and many major trading partners on-board with the multilateral sanctions campaign, the composition of Iranian trade needed to be refocused around a new set of products that could be bought and sold with a wider range of partners.

The shift toward a wider range of midsize trade partners was enabled by a concurrent one to a wider range of exported products, so that Iranian trade under sanctions was characterized by increased product complexity. Just as Iran experienced globalization between 1998 and 2008 that enabled greater geographic trade complexity, so it underwent industrialization processes that led to greater product trade complexity. By 2008, following a period of largely European investment and technology transfer, it had a greater number of manufacturing enterprises producing high-quality goods. In 1998 there were just 18 major export categories, including oil-related products, from which it was earning more than $25 million in annual export revenue. By 2008, that number was 63. Production of these goods required increased imports of raw materials and intermediate goods, such as parts and machinery, a need reflected in growth in the number of major import categories. In 1998, there were 49 in which Iran was spending more than $25 million a year. By 2008, there were 187.

The trade story is closely linked to the fortunes of the manufacturing sector under sanctions. The change in product complexity can be linked to key trends identified in firm-level analysis of Iranian manufacturing and the impact of the 2012-2013 sanctions. That analysis concluded that the financialized sanctions imposed in 2012 — similar in impact to the sanctions re-imposed by the Trump administration in November 2018 — proved “extremely costly for Iran’s manufacturing firms in terms of production and value added,” a finding consistent with the stagnation evident in Iran’s overall trade during sanctions. However, in a sign of resilience, “exit rate has not been particularly high and employment has been maintained” [12].

Many Iranian manufacturers, particularly large firms, have been able to sustain production and employment because the shock to import and export of key product categories has been smaller than the shock to overall trade — affordability seems a greater challenge than availability. When looking to the 15 product categories with the highest average import and export value between 2008 and 2018, the industrial nature of Iranian product complexity becomes clear. The largest import categories include inputs for big automotive and metals industries, as well as food products, including maize (used in producing animal feed) and wheat (processed into flour). Imports of pumps, valves and tubing, used in a wide range of industrial applications, particularly the petrochemical sectors, also point to the industrial basis for the composition of Iranian imports. Perhaps unexpectedly for a country that has endured economic hardship, gold is a major Iranian import. This is because gold and its manufactures are important stores of value during times of rising inflation. Imports of gold grew in response to demand. Given the importance of these items, it is no surprise that extraordinary efforts were made to sustain imports in the face of sanctions, which first became significant between 2008 and 2014.

The total value of imports across these 15 categories rose from an average of $9.2 billion in the three years through 2008 to $15.1 billion in the three years through 2014 — a 65 percent increase. In the three years through 2018, the total value of imports across these categories was $12 billion.

The ability to sustain imports of these major product categories in the face of sanctions pressure was critical for industrial firms seeking to sustain output. The largest non-oil export categories include products related to Iran’s petrochemical industry, such as polymers and fertilizer, as well as products related to the mining and metals industry, such as ores and semi-finished goods. Because the analysis of these categories is drawn from trade data and not production data, the significance of food and consumer goods, which are primarily exported to regional markets for which product-level data is not readily available, is not captured. Generally speaking, Iran’s key export categories reflect products that require certain degree of processing or manufacturing, and therefore depend on the availability of imported raw material and intermediate goods. Here, the growth observed in the total value of the 15 largest import categories mirrors the growth in largest export categories. The aggregate value of these 15 export product categories rose from an average of $5.6 billion in the three years through 2008, to $10.7 billion in the three years through 2014—growth of 91 percent. In the three years through 2018, the total value of exports across these categories was $10.5 billion.

Iran’s economic resilience has also resulted from the ability to generate new export revenue through the sale of new, non-oil products. Again, firm-level research identifies a kind of industrial restructuring that contributed to the emergence of greater product complexity in Iranian trade. It observes that value added shares have shifted “toward industries that rely heavily on local natural resources, and away from industries that dependent more on imported inputs and technology” [13]. While consideration of imported inputs is important, the observed shift toward manufacturing of chemical, metal and food products directly corresponds to the product categories that registered the greatest growth in total export value between 2008 and 2018. These goods are among those most in demand in Iran’s regional markets such as Iraq and its key trade partners such as China.

Further study is needed to examine the mechanisms through which trade complexity emerged as part of a virtuous cycle of industrial restructuring and to understand the firm-level drivers of this cycle. Iran’s economic resilience under sanctions reflects adaptations in the manufacturing sector that both contributed to and resulted from changes in the geographic and product complexity of trade. Recently, its manufacturing sector has demonstrated a remarkable ability to grow under the Trump administration’s maximum pressure sanctions, expanding for most of 2019 and until the COVID-19 crisis. In short, the sector has been an engine of economic resilience, because of its ability to generate non-oil export revenue [14].

V. RESILIENCE IS COMPLEX

The analysis in this paper challenges the conventional wisdom that the multilateral and unilateral sanctions imposed on Iran since 2008 have isolated it from the global economy. Looking to the changing composition of Iranian trade, it becomes clear that by 2008, the economy was sufficiently industrialized and globalized so that sanctions’ predominant impact – a significant fall in oil revenue – was less deleterious than widely expected. A study of Iran’s export-led response to sanctions pressure concludes: “Due to an increasingly globalized economy, alternative destinations exist for exporters affected by export sanctions. In other words, export deflection can compensate export destruction and, thus, should not be ignored” [15].

Yet, to the degree that Iran’s economic resilience is derived from increasingly complex trade relationships and by extension a more complex industrial base, significant vulnerabilities persist, particularly in banking and logistics. Iran’s push to increase trade complexity has in many respects defied isolation from the global economy. But while its goods continue to be bought and sold, these flows depend on atrophied banking and logistics networks. Since the imposition of financialized sanctions in 2012, Iran’s banking system has been significantly isolated; just a handful of institutions remain connected to the global payments messaging system SWIFT. Despite their connections, these banks are generally unable to send or receive direct payments from all but a few banks in Europe, the Middle East and East Asia which maintain direct correspondent banking links with Iran for humanitarian trade. The Trump administration has been considering new sanctions that would sever even these ties [16]. Similarly, few major international shipping lines serve Iran in the face of U.S. secondary sanctions, meaning that it is highly dependent on its own state-owned shipping line, IRISL, which is unable to berth in many global ports, as well on smaller shipping lines with less routine and therefore more expensive service.

Trade complexity has emerged despite the significant banking and logistics challenges. These challenges have been overcome through increased reliance on intermediation. Banking sees Iranian firms maintain accounts at banks in third countries through which they process payments. Logistically, Iran increasingly relies on re-export through countries such as the UAE and Turkey to acquire goods manufactured elsewhere. The same adaptability demonstrated by the shift to new trade partners and product categories at the macro level can also be observed at the level of specific banking channels and supply chains. Complexity thus renders the networks that underpin trade more resilient.

However, like any complicated network, the banking and logistics channels on which Iran depends are vulnerable to disruption. For example, the pressure of U.S. sanctions on third countries such as Turkey can impact Iran’s ability to do the financial transactions necessary for trade with a much wider range of countries. This was the case during the U.S. prosecution of executives at Turkey’s state-owned Halkbank for sanctions violations. Halkbank’s subsequent move to reduce its Iran exposure created a financial bottleneck on Iranian trade with Europe, even in sanctions-exempt humanitarian trade [17]. Similar pressure has seen the Bank of Kunlun, the institution at the heart of China-Iran trade, inform clients that it would only facilitate a much narrower range of Iran-related transactions [18]. These disruptions can leave Iranian firms scrambling for new ways to facilitate the flow of goods and money. So far, they have proven adept at creating new channels and redundancies that enable them to respond to disruptions and mitigate vulnerabilities inherent to trade complexity under sanctions.

But these mitigation efforts, even if successful, are not without costs. Intermediation in both banking and logistics introduces additional transaction costs for even basic trade. Add to this that financial institutions and logistics companies will often charge a premium for facilitating Iran-related trade, and it becomes clear why Iranian importers and exporters face rising costs that have their own deleterious impact on the economy. In the case of imports, rising prices are passed on to consumers, creating inflationary pressure. In the case of exports, firms must sacrifice their margins to remain cost competitive in global markets.

The financial and logistical uncertainties also reduce investment incentives, as any event could create long-term trade disruptions. COVID-19 was one such event. Its impact on the economy was magnified by Iran’s integration into regional and global supply chains. In short, Iranian firms remain committed to trade as a means to ensure their survival, but the resilience afforded by complexity does not itself equate to the kind of stability that enables investment and thereby growth.

VI. CONCLUSION

It is debatable whether the economic stagnation Iran has experienced under multilateral sanctions deserves to be described as a period of economic resilience. Had trade been allowed to develop without sanctions, increased complexity would certainly have been an expected outcome, and the value of trade would have been significantly higher. Still, sanctions did not prevent the emergence of trade complexity.

The question, however, is whether economic development that has persisted under sanctions – whether in trade or other domains – is sufficient. The deficit between Iran’s current level of economic development and the development that might have reasonably been projected prior to sanctions looms large in political discourse on the economy. Citizens expect their economic fortunes to improve over time, so in domestic political terms, stagnation is an unsustainable outcome. But when considering that sanctions policy, particularly the Trump administration’s “maximum pressure,” is intended to coerce Iran, through economic contraction, perhaps even to outright collapse, stagnation appears a sufficient outcome to declare the country’s global trade resilient, though the picture varies across insensitive, somewhat sensitive and highly sensitive countries.

From the perspective of sanctions policy, it is also significant that Iran has sought to achieve economic resilience by increasing its economic and thereby political exchanges with the international community. It has rejected efforts to cast it as a pariah state and has developed deeper economic relations with insensitive and somewhat sensitive countries, while essentially seeking to preserve ties to highly sensitive countries, particularly for imports. Sanctions have in important respects integrated Iran more deeply with the global economy and attuned its policymakers more fully to the complexities of globalized trade and the banking and logistics networks that underpin that trade.

There are two key implications for how Iran might respond to possible new negotiations with the U. S. First, because of the adaptability of its trade relationships, Iran has demonstrated greater economic resilience than widely assumed. Secondly, its efforts to sustain integration with the international economy and necessary economic development give the international community more opportunities to incentivize Iran to a new diplomatic outreach. Iranian industries exhibit high responsiveness to sanctions relief with respect to growth in non-oil exports [19]. Should the U.S. lift sanctions, the Iran that experiences relief will no longer be dependent exclusively on oil exports. Iranian and Western policymakers ought to embrace the opportunities presented by Iran’s new economic complexity.

APPENDICES

ENDNOTES

See, for example, César Hidalgo, and Ricardo Hausmann. “The Building Blocks of Economic Complexity.” PNAS 106, no. 26 (30 June 2009). https://www.pnas.org/ content/pnas/106/26/10570.full. pdf.

“Non-Oil Trade of Iran in the Year 1398. , Tehran Chamber of Commerce, May 2019. http://www.tccim.ir/Images/Docs/1193.pdf.

Jahangir Amuzegar, “Iran’s 20-Year Economic Perspective: Promises and Pitfalls.” Middle East Policy 16, no. 3, 14 (September 2009). https://mepc.org/journal/ irans-20-year-economic-perspective-promises-and-pitfalls.

“Iran blasts West’s embargo as ‘economic war’”. Al Jazeera, 5 January 2012.

Scott Peterson, “Iran’s Presidential Candidates Debate Justice and a ‘Resistance Economy’,” Christian Science Monitor, 31 May 2013

Bijan Khajepour, “Decoding Iran’s ‘Resistance Economy,” Al Monitor, 24 February 2014.

Ray Takeyh, “Iran’s ‘Resistance Economy’ Debate,” Council on Foreign Relations, 7 April 2016.

Parviz Alizadeh and Hassan Hakimian, Iran and the Global Economy: Petro Populism, Islam and Economic Sanctions (Routledge, 2013)

9. Trade data from UN COMTRADE (accessed via World Integrated Trade Solution) can be considered reliable for the countries in the highly sensitive and somewhat sensitive categories. For Iran’s regional trade partners included in the insensitive category, UN data is, where available, likely an underestimation of total trade due to the informal nature of much of what occurs at the Iranian border. The UN COMTRADE database is incomplete regarding Iraq and Afghanistan, for which data from IRICA, Iran’s customs administration, has been used. This data is recorded according to the Iranian calendar year, so data for 2009 included in this analysis reflects the Iranian calendar year 1388, which began in March 2009.

10. “Regional Economic Outlook: Middle East and Central Asia,” International Monetary Fund, October 2020. https://www.imf.org/ en/Publications/REO/MECA/ Issues/2020/10/14/regional- economic-outlook-menap-cca

11. “China-Iran Trade Report-September 2020,” Bourse & Bazaar, 24 October 2020. https://www. bourseandbazaar.com/china-iran-trade-reports/september-2020.

12. See Salehi Esfahani, SAIS Paper

13. Salehi Esfahani, op.cit.

14. PMI Data Source

15. Jamal Haidar, “Sanctions and Export Deflection: Evidence from Iran,” Economic Policy, April 2017, pp. 319–355.

16. Motevalli, Golnar, “U.S. Sanction Plan for Iran Would Imperil Drug, Food Imports,” Bloomberg. 29 September 2020. https:// www.bloomberg.com/news/articles/2020-09-29/u-s-sanctions-plan-for-iran-would-imperil- food-and-drug-imports.

17. Yinanç, Barçin, “How will Turkey trade with Iran with sanctions back and Halkbank on target?,” Hurriet Daily News, 10 July 2019. https://www.hurriyetdailynews. com/opinion/barcin-yinanc/how-will-turkey-trade-with-iran-with-sanctions-back-and-halkbank-on-target-134372

18. Motamedi, Maziar, “Policy Change at China’s Bank of Kunlun Cuts Iran Sanctions Lifeline,” Bourse & Bazaar. 2 January 2019. https://www.bourseandbazaar.com/ articles/2019/1/2/policy-change-at-chinas-bank-of-kunlun-cuts-sanctions-lifeline-for-iranian-industry

19. Dadpay, Ali, and Saleh Tabrizy. “Political Agreements and Exporting Activities: An Empirical Assessment of the Effects of the JCPOA Agreement on Iran’s Exports.” Comparative Economic Studies, September 7, 2020. https://link.springer.com/ article/10.1057%2Fs41294-020- 00136-x.

ABOUT THE AUTHOR

Esfandyar Batmanghelidj is the Founder and CEO of the Bourse & Bazaar Foundation, a think tank focused on advancing economic diplomacy, economic development, and economic justice in the Middle East and Central Asia, and particularly Iran. His scholarship on Iran’s political economy, public health, and social history has been published in peer-review journals and in the Encyclopedia Iranica. He is a graduate of Columbia University.

The SAIS Initiative for Research on Contemporary Iran

Johns Hopkins University Washington, DC

Copyright 2020 All rights reserved